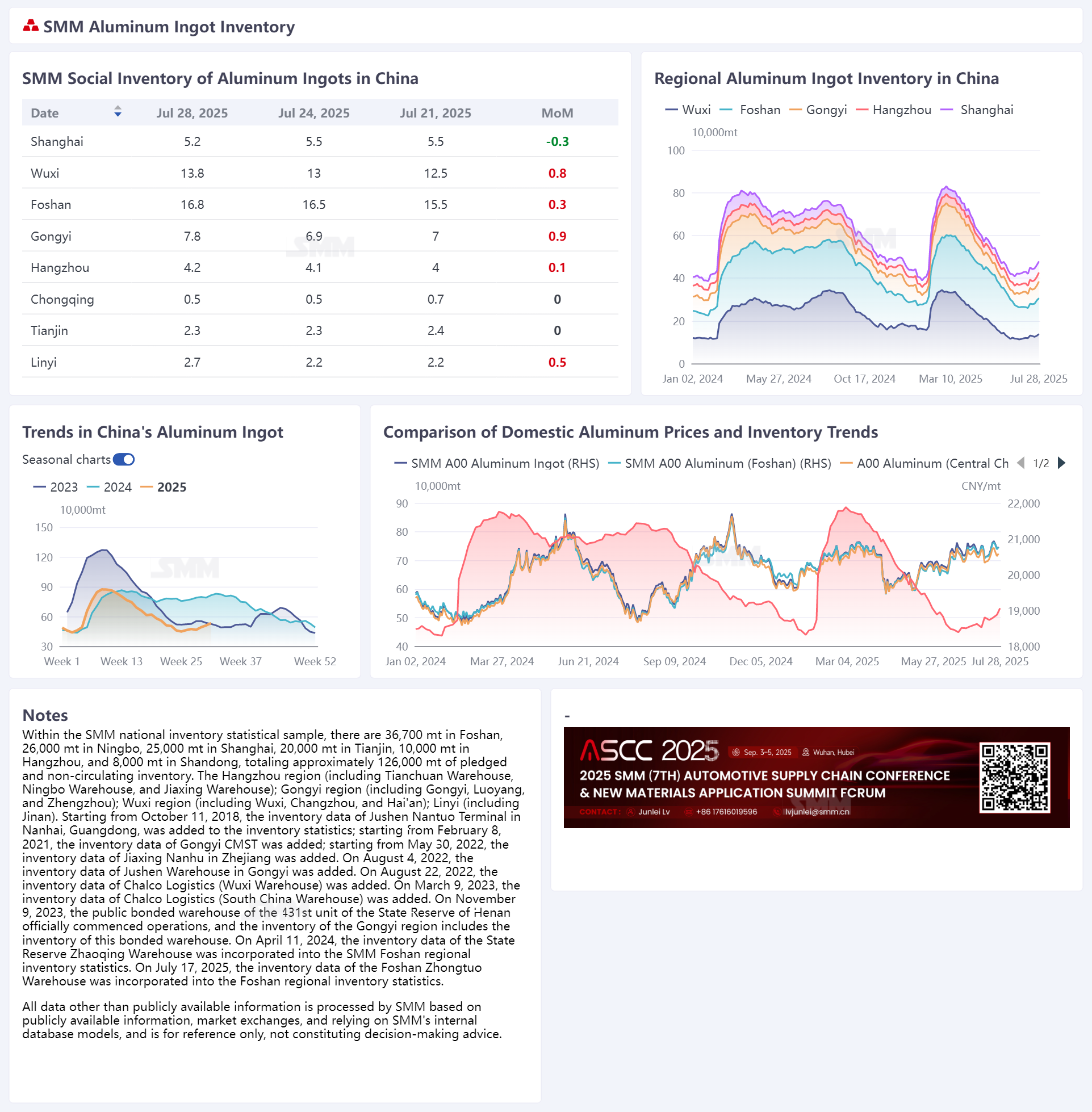

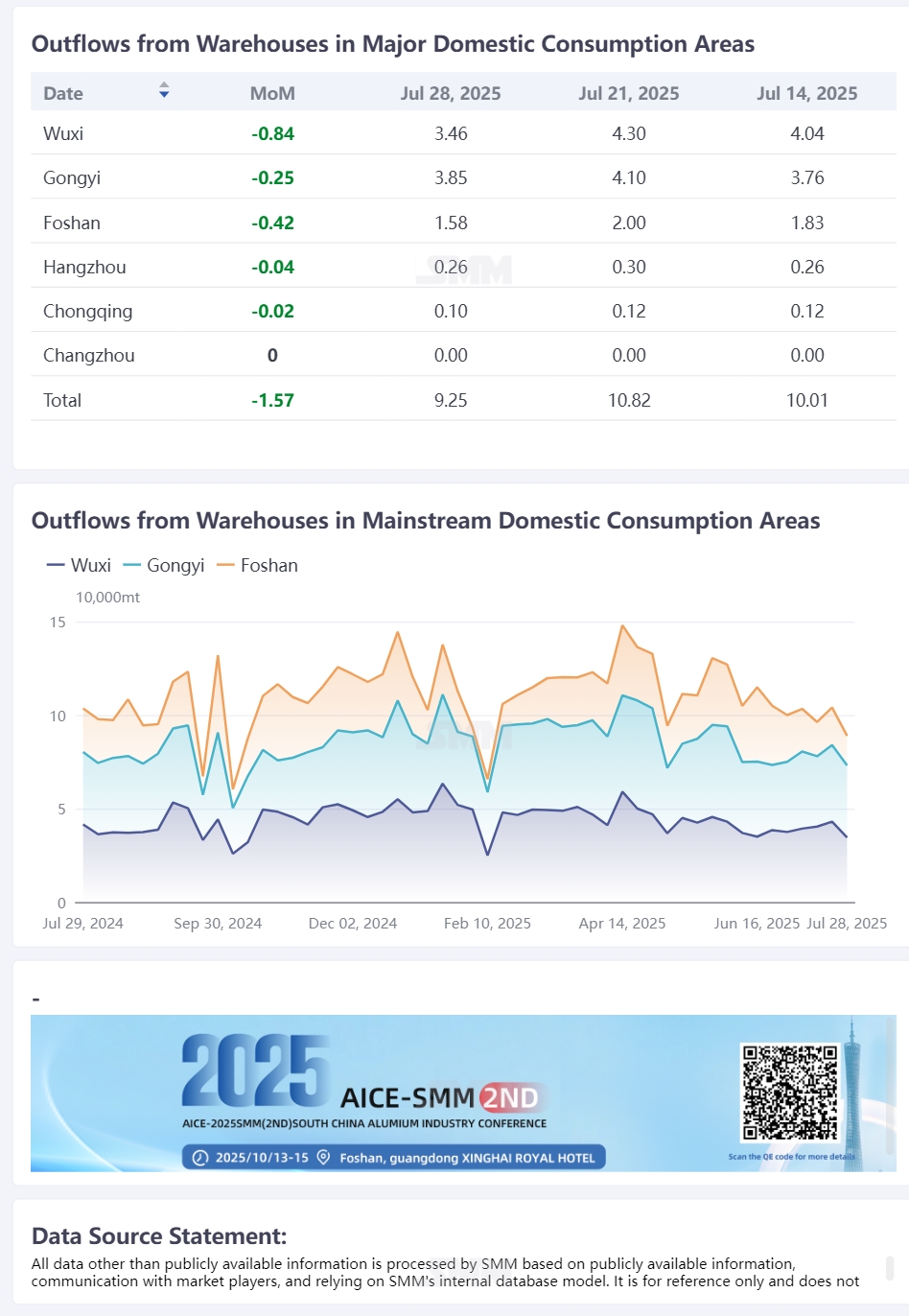

According to SMM statistics, as of July 28, the inventory of primary aluminum ingots in China's mainstream consumption areas stood at 533,000 mt, an increase of 23,000 mt compared to Thursday last week and 35,000 mt compared to Monday last week. On a YoY basis, domestic aluminum ingot inventory lost its advantageous position of being at a low level compared to the same period in the past three years. Although it still decreased by 281,000 mt compared to the same period last year, it increased by 8,000 mt compared to the same period in 2023. In terms of outflows from warehouses, the weekly outflows of aluminum ingots from major consumption areas in China in the past week were 92,500 mt, a significant decrease of 15,700 mt WoW. Excluding the impact of the Chinese New Year holiday week at the beginning of this year, the outflow data has hit a new low for the year. Entering the latter half of July, due to the decline in the proportion of liquid aluminum within the month, the supply pressure of domestic aluminum ingots remained high, and the volume of aluminum ingots in transit continued to maintain a relatively high level. The domestic inventory buildup trend continued, and it was temporarily expected that inventory would build up to 550,000-600,000 mt by the end of July.

From a regional perspective, Gongyi area was previously affected by regional price spreads, with expected and actual arrivals being relatively low, and inventory pressure being limited. Although there was an increase in the supply of goods in Qinghai area, it was mainly transported by truck to factories, and the recent decline in truck transportation costs, as well as an increase in the proportion of goods transported by truck from Xinjiang area. However, according to the latest feedback from local warehouses, the shipment and warehousing volumes of goods in Qinghai area have increased in the past week. Concentrated arrivals led to an inventory buildup of 9,000 mt on Monday this week, making it the area with the most inventory buildup over the weekend. Meanwhile, the main destinations of goods from Xinjiang area are currently primarily in east China. Coupled with the sufficient supply of aluminum ingots in north China, the arrival volume and inventory buildup pressure in east China may continue to increase in the near future. It is worth noting that with the significant increase in the supply of aluminum ingots in south-west China since the latter half of July, Foshan area has become the main contributor to inventory buildup among domestic mainstream consumption areas. However, with the resumption of production at some rod factories in Guangxi area that had previously suspended or reduced production, the arrival pressure in South China may slightly ease by the end of July and the beginning of August.

Looking ahead, due to the decline in the proportion of liquid aluminum within the month, the supply pressure of domestic aluminum ingots remains high, and the volume of aluminum ingots in transit continues to maintain a relatively high level. Meanwhile, after excluding holiday factors within the year, the outflow data in the past week has hit a new low for the year. Under the influence of strong supply and weak demand, the short-term inventory buildup pattern of aluminum ingots has not changed, and continuous inventory buildup is expected to continue until the delivery of the August contract (i.e., mid-August). Coupled with the gradual fading of the low inventory advantage of domestic aluminum ingots, it may exert significant pressure on the performance of aluminum prices in the next half-month. However, considering that August is approaching, with the "September-October peak season" approaching, there may be expectations for a rebound in the proportion of liquid aluminum. Additionally, the downstream's adaptability to current prices has improved. After the pullback of aluminum prices from highs, the pace of inventory buildup may slow down marginally. It is necessary to closely monitor the rhythm of concentrated arrivals and the release of downstream demand.